Black Knight: Number of Homeowners in COVID-19-Related Forbearance Plans Falls for First Time Since Crisis Began; 8.9% of All Mortgages Now in Forbearance

- The McDash Flash suite from Black Knight leverages daily, loan-level data to provide market participants with the most current view of the forbearance and mortgage performance landscape

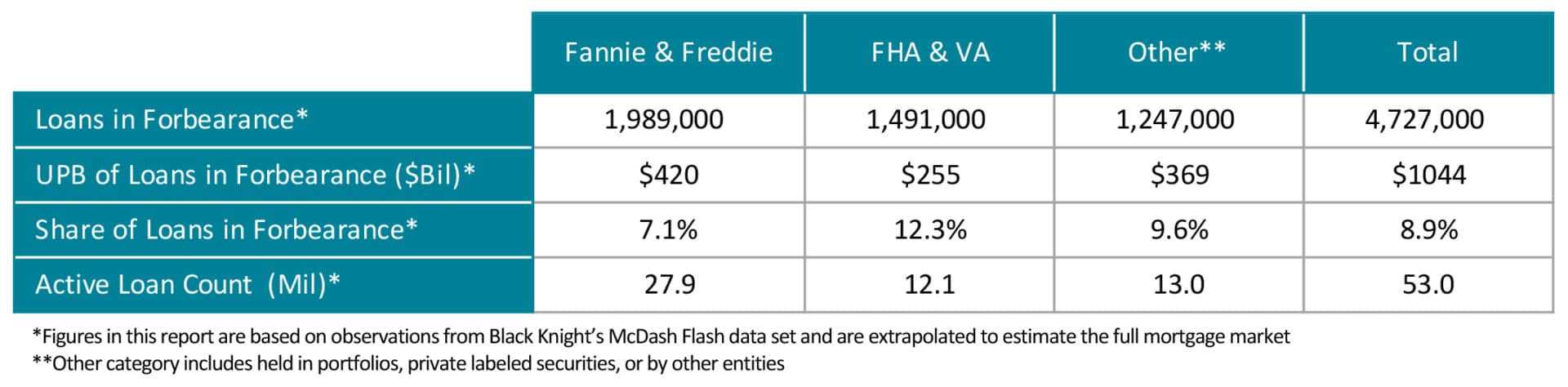

- According to the McDash Flash Forbearance Tracker, as of June 2, 2020, 4.73 million homeowners – or 8.9% of all mortgages – are in COVID-19 mortgage forbearance plans

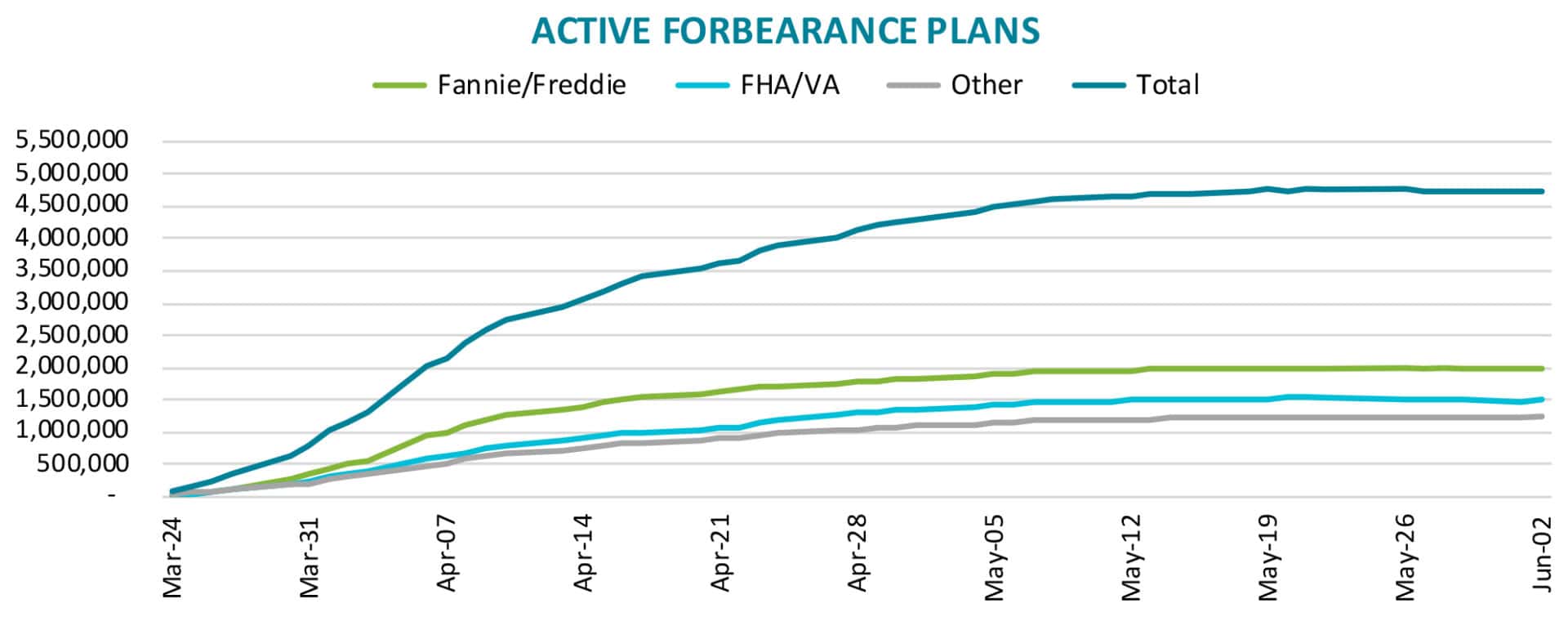

- Active forbearance volumes decreased by a net 34,000 over the past week, marking the first weekly decline since the crisis began

- A decline of 43,000 forbearances among government-backed mortgages from May 26 to June 2 was partially offset by an increase of 9,000 forbearances among mortgages in bank portfolios and private-label securities

- According to the McDash Flash Payment Tracker, as of May 26 a significantly lower share of homeowners in forbearance had remitted May payments (22%) than did in April (46%), pointing to another likely rise in the delinquency rate for May

JACKSONVILLE, Fla. – June 5, 2020 – Black Knight, Inc. (NYSE:BKI) continues to monitor the impact of the COVID-19 pandemic on the U.S. mortgage market, tracking loan-level forbearance and performance data on a daily basis through its McDash Flash data set and the McDash Flash Payment Tracker. According to Black Knight CEO Anthony Jabbour, improvement was seen in the number of homeowners in forbearance for the first time since the CARES Act has gone into effect.

“After rising sharply in April and then leveling off toward the end of May, the number of American homeowners in forbearance plans has now decreased for the first time since the crisis began,” said Jabbour. “There were a net 34,000 fewer homeowners in forbearance as of June 2. The decline was actually greater among government-backed mortgages, which saw 43,000 fewer total forbearance plans than last week, but this was partially offset by an increase of 9,000 new plans on mortgages held in bank portfolios and private-label securities.”

The McDash Flash Forbearance tracker shows that the 4.73 million loans in forbearance represent 8.9% of all active mortgages and account for a little over $1 trillion in unpaid principal. An estimated 7.1% of all GSE-backed loans and 12.3% of FHA/VA mortgages are now in forbearance.

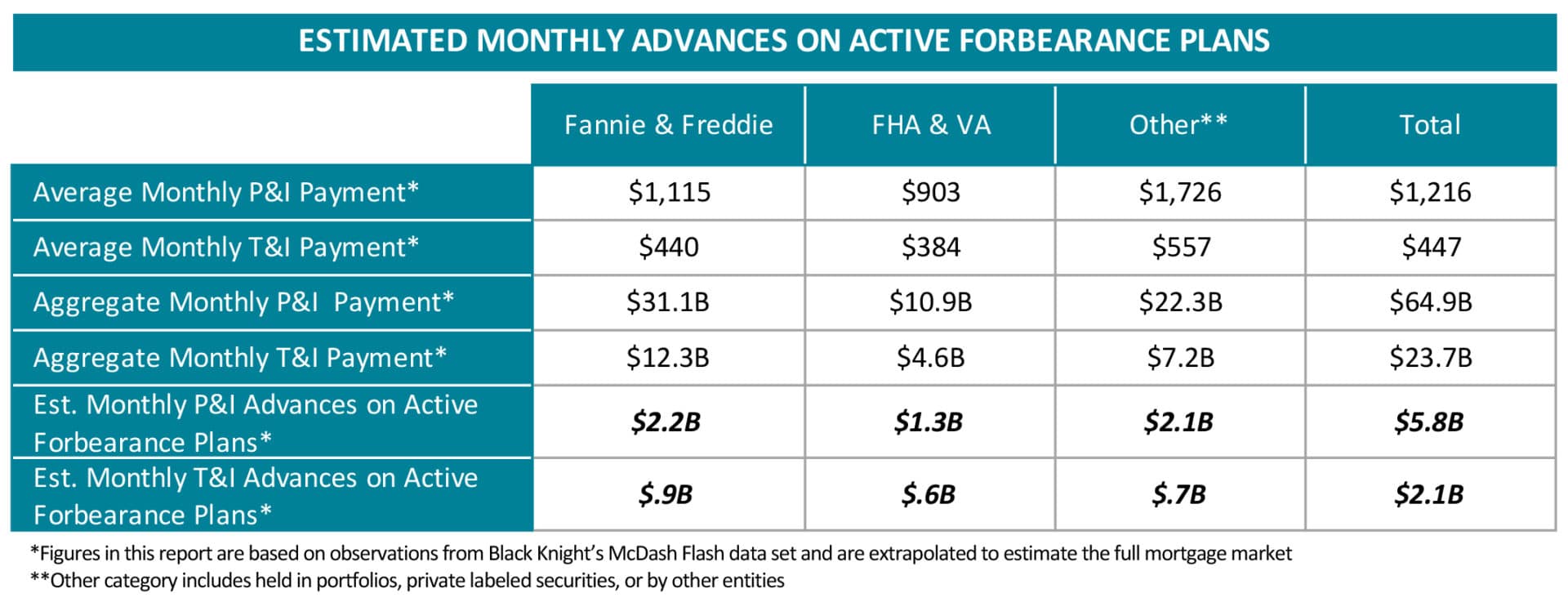

The decline is driving a shift in servicer focus from forbearance pipeline growth to forbearance pipeline management. Black Knight’s daily McDash Flash data allows subscribers to track outstanding populations, payment activity, upcoming forbearance expirations and overall forbearance performance on a near-real-time basis. Likewise, Black Knight’s Loss Mitigation solution, integrated with the industry-leading MSP servicing system, provides essential functionality for managing not only the forbearance period, but the millions of loan workouts and modifications that are likely to follow.

“While this decline is welcome news,” Jabbour continued, “there are still concerning signs in the data. According to Black Knight’s McDash Flash Payment Tracker, far fewer homeowners in forbearance remitted May payments than did in April. If that trend holds true through the end of the month, the market should be prepared for another likely rise in the delinquency rate for May. Also, expanded unemployment benefits are scheduled to end on July 31. It remains to be seen how that will impact both forbearance requests and overall mortgage delinquencies.”

Like McDash Primary data, McDash Flash data is anonymous and does not contain any nonpublic personal information (NPI) or personally identifiable information (PII), but can be benchmarked and/or extrapolated up for a full-market picture.

As of June 2, 2020, the McDash Flash Forbearance Tracker found the following:

Moving forward, Black Knight will continue to provide weekly McDash Flash Forbearance Tracker updates via Vision, the Black Knight blog. Those interested in staying up-to-date on industry developments are encouraged to visit the blog for more information in the coming days and weeks.

About Black Knight

Black Knight (NYSE: BKI) is a leading provider of integrated software, data and analytics solutions that facilitate and automate many of the business processes across the homeownership lifecycle.

As a leading fintech, Black Knight is committed to being a premier business partner that clients rely on to achieve their strategic goals, realize greater success and better serve their customers by delivering best-in-class software, services and insights with a relentless commitment to excellence, innovation, integrity and leadership. For more information on Black Knight, please visit www.blackknightinc.com.

Forward-Looking Statements

This press release contains forward-looking statements that involve a number of risks and uncertainties. Statements that are not historical facts, including statements regarding expectations, hopes, intentions or strategies regarding the future are forward-looking statements. Forward-looking statements are based on Black Knight management’s beliefs, as well as assumptions made by, and information currently available to, them. Because such statements are based on expectations as to future financial and operating results and are not statements of fact, actual results may differ materially from those projected. Black Knight undertakes no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise.

The risks and uncertainties that forward-looking statements are subject to include, but are not limited to:

- changes in general economic, business, regulatory and political conditions, including those resulting from pandemics such as COVID-19, particularly as they affect foreclosures and the mortgage industry;

- the outbreak of COVID-19 and measures to reduce its spread, including the effect of governmental or voluntary actions such as business shutdowns and stay-at-home orders;

- security breaches against our information systems;

- our ability to maintain and grow our relationships with our clients;

- changes to the laws, rules and regulations that affect our and our clients’ businesses;

- our ability to adapt our services to changes in technology or the marketplace or to achieve our growth strategies;

- our ability to protect our proprietary software and information rights;

- the effect of any potential defects, development delays, installation difficulties or system failures on our business and reputation;

- risks associated with the availability of data;

- the effects of our existing leverage on our ability to make acquisitions and invest in our business;

- our ability to successfully integrate strategic acquisitions;

- risks associated with our investment in Star Parent, L.P. and the operation of its indirect subsidiary, The Dun and Bradstreet Corporation; and

- other risks and uncertainties detailed in the “Statement Regarding Forward-Looking Information,” “Risk Factors” and other sections of our Annual Report on Form 10-K for the year ended December 31, 2019 and other filings with the SEC.

Media Contacts

Mitch Cohen

704.890.8158

mitch.cohen@bkfs.com

Katia Gonzalez

678.981.3882

katia.gonzalez@ice.com